Earlier this month, the European Union announced an investment of €852 million ($1 billion) in six lithium-ion battery factories, which is part of the EU’s Battery Value Chain Enhancement Plan, with a total budget of €30 billion ($35 billion).

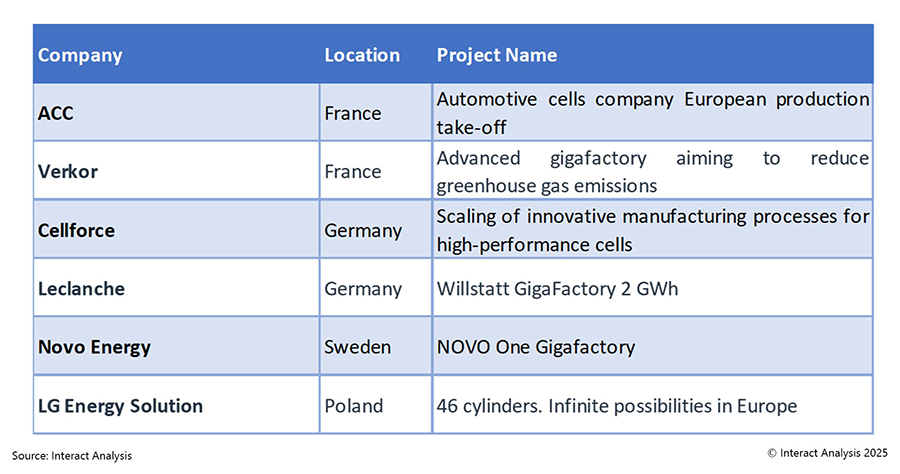

Six EU-funded battery factory projects

These projects have a combined capacity of approximately 56 GWh and are expected to be operational by 2030. The specific list of projects is as follows:  In addition to boosting Europe’s lithium-ion battery manufacturing capacity and reducing dependence on external supply chains, this investment is also part of wider technological and green transition initiatives. The focus is on innovative manufacturing technologies and low-carbon emissions. For instance, the AGATHE project is targeted at cutting emissions and drives iteration of lithium-ion battery technologies in alignment with the EU’s climate neutrality goals. The six factories receiving funding are expected to reduce greenhouse gas emissions by 91 million tons of CO₂ equivalent in the first 10 years of operation.

In addition to boosting Europe’s lithium-ion battery manufacturing capacity and reducing dependence on external supply chains, this investment is also part of wider technological and green transition initiatives. The focus is on innovative manufacturing technologies and low-carbon emissions. For instance, the AGATHE project is targeted at cutting emissions and drives iteration of lithium-ion battery technologies in alignment with the EU’s climate neutrality goals. The six factories receiving funding are expected to reduce greenhouse gas emissions by 91 million tons of CO₂ equivalent in the first 10 years of operation.

However, this investment also has certain drawbacks. For one, the 56 GWh capacity is relatively limited and cannot meet market demand in European sectors such as electric vehicles and energy storage. This means it will not alter reliance on external supply chains in the short term. Secondly, while the projects stress “innovation,” they depend on “technical maturity” criteria assessed by independent experts. There is also uncertainty surrounding the scaling up of some technologies–such as innovative manufacturing processes for high-performance batteries–to mass production, which may lead to delays.

Furthermore, the projects are concentrated in a handful of countries in Western and Central Europe, leaving parts of Southern and Northern Europe without coverage, and the investment provides no support for raw materials or recycling programs.

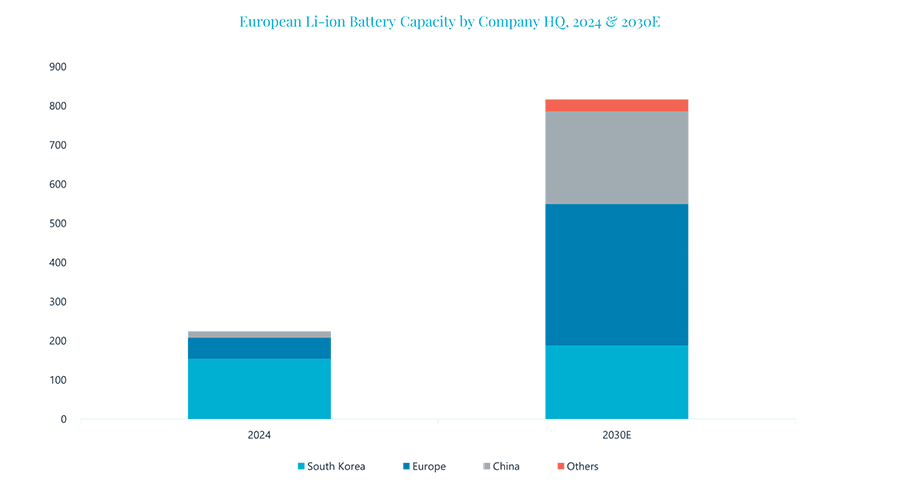

Europe’s lithium-ion battery capacity is expected to exceed 800 GWh by 2030

Based on Interact Analysis’ Global Lithium-ion Battery Plant Tracker , Europe’s lithium-ion battery capacity landscape is undergoing dynamic changes. As of the second quarter of 2025, the total announced capacity of lithium-ion battery projects in Europe (excluding battery packs and solid-state batteries) exceeded 1.9 TWh. However, due to factors such as the slowdown in the growth of electric vehicle demand and higher-than-expected complexity of supply chain construction, some projects have encountered setbacks. In fact, projects by companies such as NorthVolt have stagnated or even stopped.

As of the end of 2024, lithium-ion battery capacity in Europe exceeded 220 GWh. Factories built by South Korean battery companies (LGES, SK On, Samsung SDI) in Hungary, Poland, and other countries contributed nearly 70% of the total, highlighting the dominance of foreign capital in the sector. According to Interact Analysis, lithium-ion battery capacity in Europe is expected to reach more than 800 GWh by 2030. By then, the proportion of capacity accounted for by European domestic enterprises is expected to rise to 43%, Chinese enterprises will comprise about 29%, while the proportion represented by South Korean enterprises will shrink to 23%.

The regional capacity landscape is expected to see a clear trend away from foreign capital dominance towards domestic investment and diversified competition.  The proportion of capacity represented by European domestic enterprises is expected to rise to 43% by 2030

The proportion of capacity represented by European domestic enterprises is expected to rise to 43% by 2030

Final thoughts

It’s worth noting that compared with the first-mover advantages built up by Chinese and South Korean companies in the lithium-ion battery sector, European firms still face significant challenges when it comes to large-scale battery capacity expansion. Not only did European enterprises enter the market later, but they must also grapple with practical hurdles such as the high complexity of supply chain development and the stagnation of some projects due to fluctuating demand or insufficient technical maturity. While the EU has created favorable conditions for local enterprises through policy support, achieving late-mover advantages and securing a solid position in the domestic market will require the alignment of multiple factors.

On the one hand, the demand for electric vehicle electrification in Europe needs to recover to provide a market foundation that will absorb the additional capacity. On the other hand, policy dividends must be effectively translated into tangible support, forming a closed-loop system that spans technological R&D to industrial chain collaboration. Additionally, enterprises need to overcome large-scale production bottlenecks and convert innovative achievements into stable output capacity to truly carve out a place in the future landscape.