ISA provides technical resources and standards to help industrial automation professionals advance their careers and the field. We enable automation professionals worldwide to solve problems and enhance their skills by bringing people together to create new technologies and share best practices with future automation professionals.

We attract over 140,000 unique automation professionals monthly, making us the premier online content provider and the only dedicated electronic magazine in the automation industry.

Global supply chains are in another period of high stress and are becoming increasingly complex.

In April 2025, the Global Supply Chain Stress Index saw a dramatic rise as the dual shocks of tariff measures and heightened policy uncertainty disrupted global trade flows. Rapidly changing trade rules and unclear policy direction generated significant hesitation among supply chain managers, forcing companies to delay investment decisions, reroute shipments and reassess sourcing strategies. This marked a sea change following the relative calm seen in 2023 and early 2024. From 2025 into 2026, stress has remained elevated, driven not only by ongoing geopolitical tensions but also, increasingly, by structural trade fragmentation and persistent tariff uncertainty, which continue to raise costs, extend lead times and increase operational complexity across global supply networks.

Greater supply chain complexity tends to be associated with higher revenue and capacity requirements for major third-party logistics (3PL) providers, as supply chain challenges encourage more companies to outsource logistics to specialized partners. When the Global Supply Chain Stress Index climbed from roughly 0.5 in 2020 to above 2.0 in 2022, combined quarterly revenues for DHL Group, Kuehne + Nagel, CEVA Logistics, and A.P. Moller Maersk doubled from about ~€32Bn to nearly €58Bn. As supply chains become ever more complex, lead times become longer, volatility rises, and operational risks grow, making in-house logistics more difficult to manage. In response, more and more companies appear to be outsourcing supply chain operations to 3PLs.

This trend is reflected in our warehouse construction forecast, which shows 3PL providers expanding faster than the overall market. While the total warehouse construction index declined from 107 in 2022 to 103 in 2024 and will remain largely flat through 2030, the 3PL index rebounded strongly, rising from 103 in 2024 to 112 in 2026.

This divergence indicates that 3PL warehouse investment remains structurally elevated despite weaker overall construction activity. CEVA Logistics, for instance, is developing a new warehouse in Singapore that will increase its total warehouse footprint to around 4 million square feet. In parallel, Kuehne+Nagel has opened a new 108,000 square foot healthcare distribution centre in Germany to support complex, multi-temperature logistics flows across EMEA. Both of these companies mentioned that the need to increase their footprints was a direct result of increasing demand.

What does this mean for warehouse automation investments?

3PLs throw up the most complex challenges where the adoption of warehouse automation is concerned. This is because the nature of their operations means they rely on high flexibility, with multi-client facilities, changing SKU mixes, and shorter contracts. This translates into a demand for mobile automation that can scale or be redeployed quickly, as has been evident in recent deployments, with DHL Supply Chain expanding its partnership with Locus Robotics to deploy up to 2,000 autonomous mobile robots globally, which can be flexibly utilized during peak periods. In parallel, companies such as DSV have deployed AutoStore systems across their networks. DSV has plans for a global roll-out of automation across 20 fulfilment centres.

Advertisement

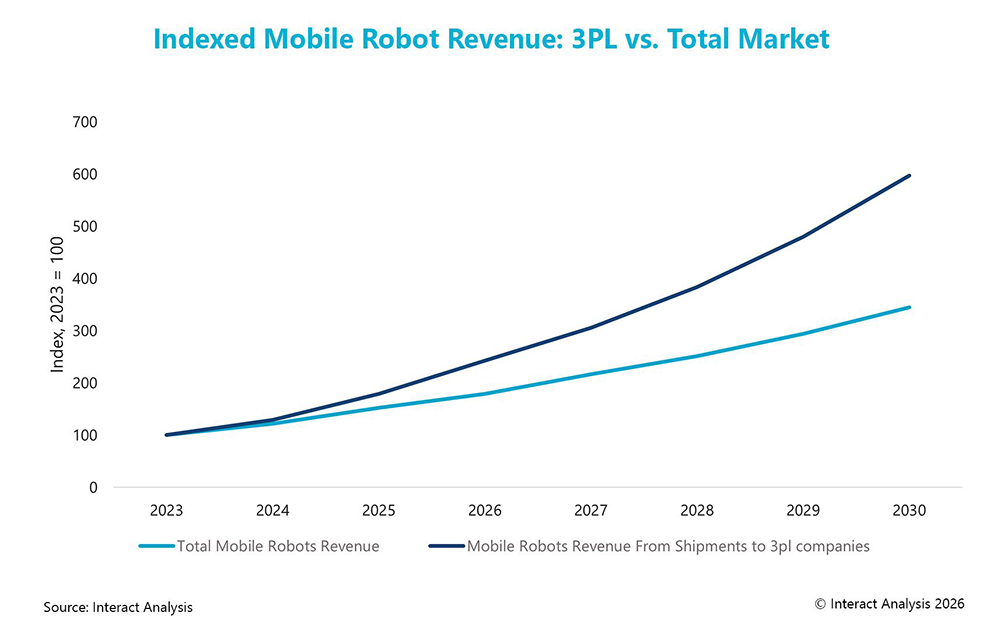

This trend is reflected in our forecast, where mobile robot revenue from 3PL customers grows significantly faster than the overall market, increasing nearly sixfold between 2023 and 2030 compared to a roughly threefold increase for the total market, highlighting the structurally rising role of 3PLs in driving mobile automation demand.

How will this affect system integrators?

A strategic convergence between 3PLs and system integrators is increasingly plausible as their value propositions begin to overlap. System integrators no longer just design automation architectures; many now deliver turnkey warehouse environments that include software, equipment, maintenance, and in some cases on-site operational support. Functionally, this moves them closer to managing the warehouse itself rather than simply enabling it. At the same time, 3PLs are investing heavily in automated facilities to improve productivity and differentiation. As automation becomes central to warehouse performance, the boundary between “operator” and “technology provider” could blur, raising a logical question: if integrators already deploy and sustain the infrastructure that runs a distribution center, isn’t it a natural next step for them to extend into logistics services? This suggests a potential shift toward more vertically integrated models where execution and automation expertise sit under the same roof.

This shift is, in fact, already visible in the market. For example, GXO Logistics acquired Invar Group to strengthen its in-house automation capabilities and move closer to system integration. At the same time, new entrants are emerging with hybrid models that combine logistics operations and automation technology. Nimble Robotics operates fully automated 3PL fulfilment services built around its own robotic systems. Similarly, GreenBox Systems is developing automated warehouse solutions paired with operational logistics services. And Winit integrates warehouse operations with proprietary automation and IT systems to manage complex global fulfilment networks.

Final thoughts

Taken together, these developments highlight that supply chain complexity is not only increasing; it is fundamentally reshaping how companies approach logistics. What was once treated as a supporting function is increasingly becoming a strategic capability, requiring scale, flexibility and technological sophistication that many companies cannot efficiently build in-house. This shift is accelerating the growth of 3PLs, driving new warehouse construction and redefining the role of automation across the supply chain. In this environment, keeping up with the latest market developments is critical, as small changes in complexity, trade policy, or demand patterns can rapidly translate into shifts in logistics strategies, investment priorities and technology adoption.

To explore the structural forces reshaping warehouse demand in greater depth, including global facility counts, footprint, labor economics and automation adoption, see our Warehouse Building Stock Database. The report delivers a comprehensive bottom-up view of the global warehouse market, quantifying scale, structure and economic value across regions, countries and end users.